The Series A Squeeze in Latin America

Why raising a Series A has become the most challenging milestone for startups in the region

One of the biggest shifts in Latin America’s startup landscape is how difficult it has become to raise a Series A.

In 2021 and early 2022, companies with ~$1M USD in ARR could close a Series A in just a few weeks. Fast forward to 2025, and the dynamic is completely different—Series A has become not just harder, but arguably the hardest milestone to reach in the startup journey.

It’s Not Just Hard—It’s a New Reality

Before we go further, let’s remember that fundraising in Latin America has always been tough. Pre-2021, there were fewer funds, less sophistication across the ecosystem, and minimal attention from international players. Even so, incredible companies were built—and some surpassed $1B USD in valuation.

But the mistake today is anchoring to the 2021-early 2022 boom as the benchmark. That was an anomaly, not the baseline. The rules have changed, and the bar has been raised dramatically.

Series A is now a proving ground not only for traction and product-market fit, but for capital efficiency, growth quality, and team resilience. In many ways, it’s become the ultimate filter.

What the Data Says

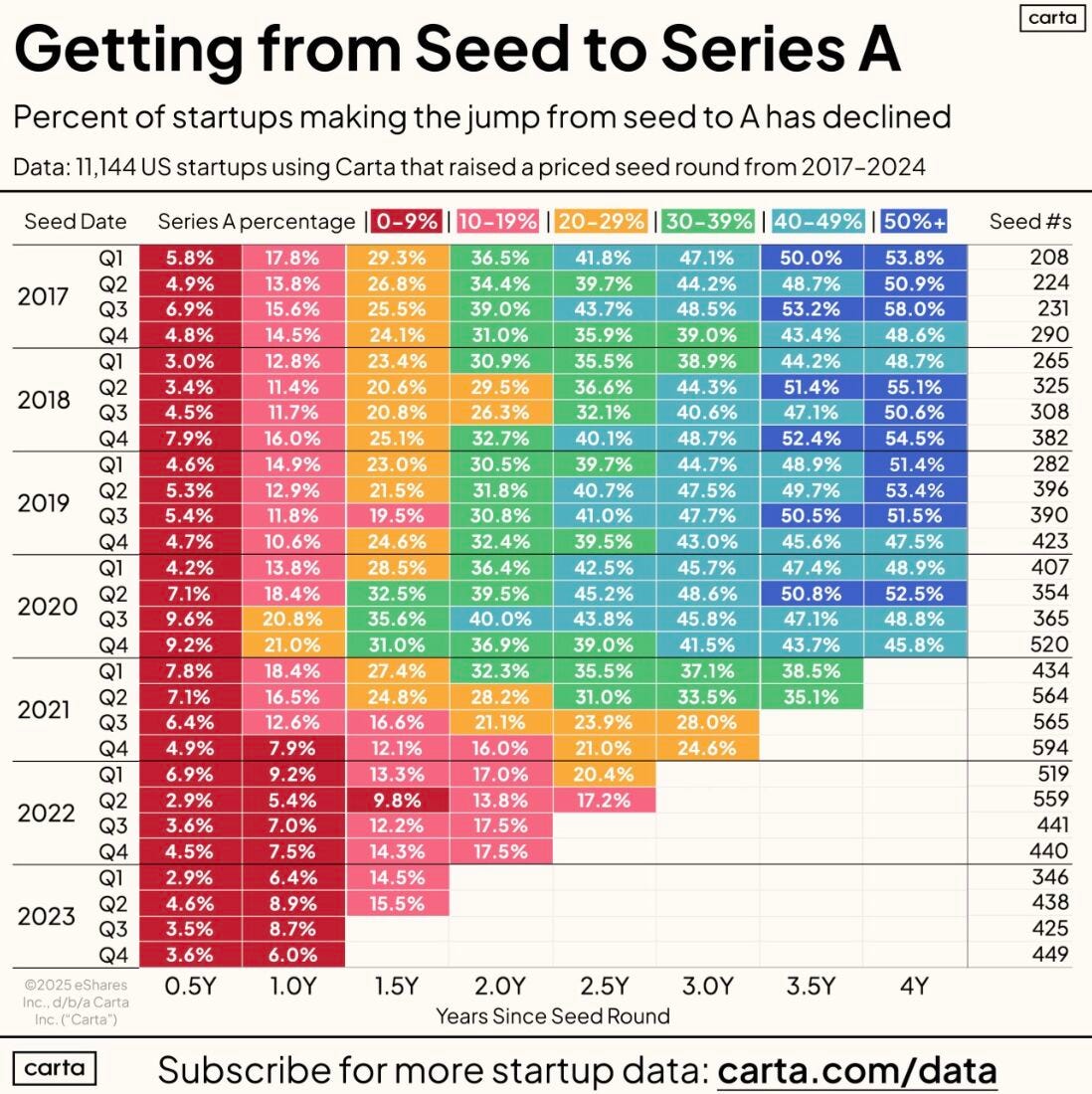

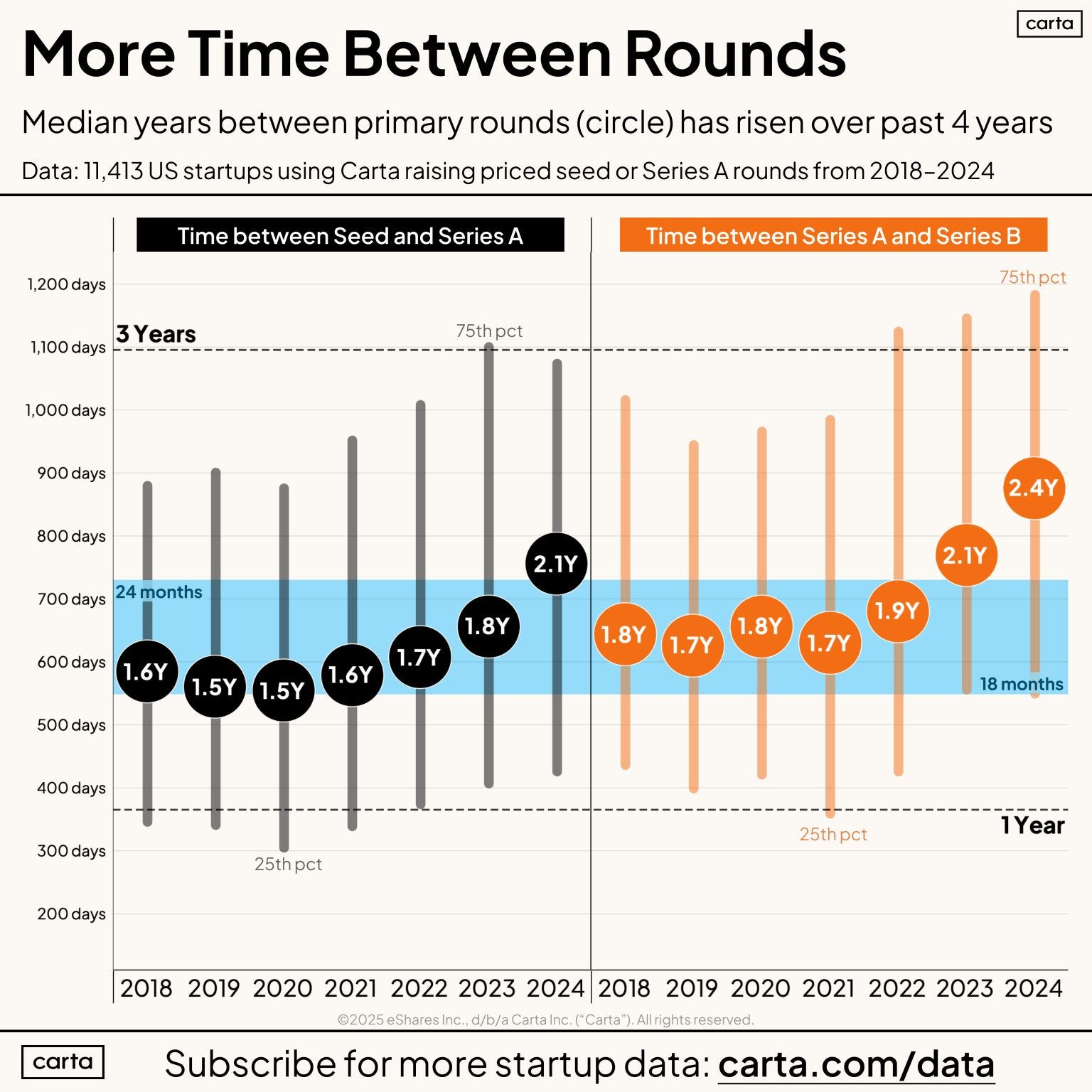

While reliable data for Latin America is scarce, Carta’s U.S. data still offers a useful lens:

In recent cohorts, less than 20% of startups raised a Series A within two years of their Seed round.

In comparison, companies seeded between 2017–2021 typically saw 30%+ success rates at that two-year mark.

Time between Seed and Series A is also steadily increasing, even for those who do manage to raise.

And this is just the U.S. — if it’s this hard in the most mature market, the situation in LatAm is likely more extreme.

Why Is This Happening?

1. Local Funds Are Running Low on Dry Powder

Many VC funds in LatAm—particularly in Spanish-speaking countries—have already deployed the majority of their investable capital. What’s left is mostly reserved for follow-on investments in existing portfolios.

Brazil stands apart. The Brazilian ecosystem is a few years ahead. Liquidity events, new rounds, and fresh fund closings are more common. While it’s not easy there either, the difference in capital availability and maturity is noticeable.

In contrast, new fund formation across the rest of the region is slow. Liquidity has dried up, LP appetite is cautious, and paper returns from the 2021 boom are weighing on performance metrics.

2. Global Investors Are Taking a Step Back

International funds have not disappeared, but they’ve reprioritized.

Many are focused on “mega trends” like AI models, defense tech, quantum computing, and biotech—sectors with limited representation in LatAm.

Startups in the region tend to focus on fintech, Industry 4.0, HR and back-office tools, or AI wrappers. These models, while impactful locally, don’t always align with the global excitement.

Add to that a lack of meaningful exits and structural liquidity issues, and Series A investing in LatAm starts to feel like an asymmetric risk play.

For global investors, it’s often easier to wait until Series B+, when the risk is lower and there's more data to underwrite a winner. While writing this post, Mendel and Felix announced their Series B, and Merama its Series C - while anecdotal evidence, international funds were willing to lead these rounds in Latam companies.

3. Series A’s Risk-Reward Profile Has Eroded

Series A has landed in an awkward middle ground:

Some funds that used to lead Series A rounds are now pivoting earlier, toward Seed and Pre-Series A, where smaller checks and earlier entry create better upside potential.

Others that traditionally focus on Series B and beyond are staying put. They have no interest in the ambiguity and risk of Series A-stage bets.

That leaves fewer funds actively writing Series A checks—and even fewer willing to take the lead. As a result, the bar keeps rising.

What Can Founders Do?

1. Accept the Timeline Shift

It won’t take weeks. It may take 6, 12, or more months to go from building your materials to seeing capital hit the bank account. Hitting the market with less than 12 months of runway is a huge gamble.

2. Build for Multiple Scenarios

Founders often aim to raise exactly what they believe is needed to get to the next stage. But the current market demands flexibility:

You may need to raise a smaller bridge.

You may need to cut burn to extend runway.

You may not be able to raise at all—and have to focus on profitability.

Build contingency plans early and pressure test them with your investors.

3. Get Creative About Who You Raise From

The traditional path—raise a clean Series A led by a well-known fund—is often not feasible. That doesn’t mean the round can’t happen:

Look to family offices, emerging managers, development banks, or sector-specific funds.

The key is finding capital aligned with your risk profile and business model—not just chasing logos.

4. Consider Skipping the “Classic” Series A

Instead of raising a full Series A, some startups are opting for a bridge that gets them to Series B in 12–24 months.

This might be 25–50% of the ideal Series A round.

It can often be led by insiders, with a few smaller new investors joining.

It’s risky and requires alignment from the board and existing cap table—but it’s being done.

In successful cases, this approach creates strong returns for investors who double down at lower valuations and allows startups to skip a crowded, uncertain funding stage.

5. Stretch Runway and Push for Profitability

While this may slow top-line growth, it reframes your fundraising narrative. Instead of raising to survive, you’re raising to accelerate. That positioning makes a huge difference when engaging with cautious investors.

It’s not the classic VC path—but these aren’t classic market conditions.

Final Thoughts

I’ve had the Series A conversation with numerous entrepreneurs recently—and I wanted to put thoughts into writing.

The goal isn’t to paint a bleak picture. It’s to be honest about where we are.

A trend to keep in mind is the emergence of Series A specific funds, its a trend that is emerging in Brazil and we could likely see it in spanish-speaking Latam soon. These funds are high conviction and high concentration, looking to cherry-pick the potential Series A companies in the region.

And most importantly, to remind everyone: this isn’t the first tough cycle.

Building a startup in Latin America was even harder in 2016, 2017, 2018, and 2019. And still, amazing companies were built. The best founders figured it out. They didn’t expect the road to be easy—they just kept walking it.

Today’s environment isn’t easy. But great startups are still being built. And for the ones that make it through this phase, the upside will be there.

Agreed; in my experience, the KPIs with which US-based startups raise (ARR) is way below what startups in LatAm are required to raise comparable rounds.

Series A risk in LatAm requires series B metrics due to lack of exits / additional risk for VC’s…

Local VC’s could be more aggressive and use their connections to increase the odds of subsequent rounds of funding (with international VC’s) but most limit to making intros vs actively facilitating those rounds… meaning only supernovas get through!

Muy útil!