Why are VCs so strict on the minimum ownership in a startup when investing?

Spoiler: (Fund) size matters!

A common source of frustration—or a happy problem, depending on how you see it—that entrepreneurs face when fundraising is figuring out the allocations for investors when closing a round.

After weeks or months of fundraising calls and meetings, endless requests, and updates to the data room, there is finally a set of terms that has been agreed upon, a lead investor, and potential co-investors. However, making everybody happy is tough, as each investor tends to have a minimum ownership threshold. If these thresholds were to be respected, the dilution for founders would be way too high.

Let’s work through an example. Please keep in mind I’m taking a few shortcuts to illustrate a point; a more detailed example would yield the same conclusion.

A startup is fundraising a $5M USD Seed Round at a $25M USD post-money valuation (20% dilution). Potential investors in the company might look something like this:

As a result, if these ownership requirements were respected, the company would receive ~$7.4M USD on the lower end of the range and ~$9.9M USD on the higher end. Assuming the pre-money valuation won't change, the dilution for the founding team would be significantly higher than originally expected.

While I won't get into how to handle or negotiate/optimize this situation in this post (expect that in an upcoming post), I've seen founders complain about this situation. I understand the frustration—a lot of work has been done and relationships developed. It is natural for the entrepreneur to want all the interested funds to participate in the round. At the same time, they need to take care of their ownership and the company’s cap table.

Common comments by founders include:

Why can't the venture capital funds be more flexible?

There will be opportunities to invest in the company in the future, so why not get in now and have a front-row seat for future opportunities?

If we become a unicorn, does it really matter how much they invest today?

To understand this situation, it is important to highlight a critical issue VC funds face: fund size dictates a significant part of the fund deployment strategy. VC follows the Power Law, which, summarized, says a small percentage of your investments will provide the vast majority of the returns. VCs understand that it is highly unlikely to invest in a company that achieves a billion-dollar-plus valuation, and as such, they want to make sure that when they hit the jackpot, that investment will at least return the whole fund. The bigger the fund, the larger that jackpot needs to be. A small fund may have a fund maker if a company achieves a valuation in the $200M or $300M USD range, while a larger fund needs a +$1B USD outcome.

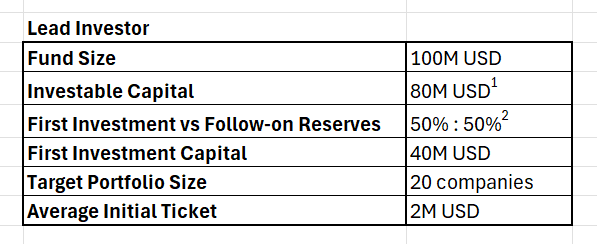

Let's deep-dive into the lead investor scenario in the example above. Once again, I'll be making a few assumptions:

Now let's look at how this investment would look (if things work out great for the company):

I'm being very generous with the ownership calculation for the sake of emphasizing the complexity of returns in VC even when things work out “perfectly.” Additional sources of dilution are likely (i.e., ESOP, Bridge Rounds, etc.), and as a result, dilution would be more aggressive.

Let's assume this may actually happen. This fund invested early in a juggernaut, hit the jackpot, and now has a unicorn in their portfolio. They own 8% of the company, and at a valuation of $1B USD, that investment is now worth $80M USD, having invested $9.5M USD in the company. While this is great news, the investment only returns 80% of the fund, and that assumption implies the fund can find liquidity at that valuation. If they tried to sell through a secondary, IF there was a buyer, there's likely to be a discount as a result of the seniority of the shares being sold and access to said liquidity. Assuming a discount of ~20%, that transaction would return 64% of the fund. I just outlined a "dream" scenario for a VC investment, and the investment doesn't yield a fund maker.3

THIS is why VCs are so strict about ownership, and the bigger the fund size, the harder the math I just outlined gets. It’s really tough to unlock returns in venture capital.

What could this fund do differently? Maybe wait another round? Sure, let's say the company keeps on this trajectory. Eighteen to twenty-four months later, the company is now worth $1.5-2B USD. Regardless of the dilution (which tends to be small at this stage), the math will work out better. However, keep in mind that waiting implies risk. What if there's an economic downturn, a pandemic, or political unrest in the main market the company operates in? Liquidity at that $1B USD valuation may never materialize.

Now, let's assume the fund is able to capture a 15% ownership at the seed stage. A similar scenario unfolds, and by the time the company achieves a $1B USD valuation, the fund owns 11-12% of the company—the math for a fund maker starts to work better this time around, even with a discount through a secondary transaction.

When initially investing in a company, VCs care more about ownership than ticket size. They would rather invest an extra $500k USD early and guarantee a larger ownership stake, which may be a gamechanger if things go well.

On the flip side, being “flexible” for the sake of getting into the deal is generally a no-go. Starting this exercise with an 5-8% ownership will yield a return under 50% of the fund size. Additionally, it’s tough to grow your ownership when a company is doing really well; new investors will have minimum ownership thresholds, and the rounds will likely be oversubscribed. Heck, sometimes it’s tough to get your pro-rata, even when there are legal documents that guarantee it.

I hope this provides some insights on why VCs act the way they do about ownership. Keep in mind what I highlighted earlier: the bigger the fund, the more strict they tend to be on ownership. A $100M USD fund has to be more strict than a $10M USD fund.

I'm estimating 20% of the fund will be used in management fees, setup costs, and operating expenses. Although a bit high (most funds are closer to 17-18%), I've seen examples that go well above 20%.

This is probably the biggest assumption in this example. Depending on the stage and focus, this could vary significantly. Using 50-50% as I believe it is in line with many funds and to keep things easy.

Other sources of liquidity would include IPO or M&A. At this point the company is a few years away from an IPO. An M&A is always on the table, but +1B USD M&As in Latam are rare (once again being generous).

Hey Patrick, I would love to do guest post with for my community VC Mx on fund economics and how it affects LATAM ecosystem specifically for founders!

Here’s my website:

mackmeyer.com